Table of Contents

ToggleCapital Gains Tax Australia Investment Property Guide: What Every Investor Needs to Know

For many Australian property investors, negative gearing is one of the most commonly used wealth-building strategies.

The concept is simple: you accept a short-term cash flow loss on your investment property because the tax benefits and long-term capital growth potential may outweigh those losses over time.

But while many investors focus on reducing their taxable income today, fewer fully understand the tax implications when it comes time to sell.

This is where Capital Gains Tax (CGT) becomes an important part of your investment strategy.

Understanding capital gains tax Australia investment property rules is essential for every property investor. Whether you’re planning to sell a rental property, refinance your portfolio, or build long-term wealth through real estate, knowing how CGT works can help you make more informed financial decisions. Whether you’re planning to sell a rental property, refinance your portfolio, or build long-term wealth through real estate, knowing how CGT works can help you make more informed financial decisions.

In this guide, we’ll explain how Capital Gains Tax works in Australia, how the 50% CGT discount applies, and what investors should consider before selling an investment property.

Table of ContentsToggle Table of ContentToggle

What is Capital Gains Tax (CGT)?

Capital Gains Tax (CGT) is the tax that may apply when you make a profit from selling an asset such as:

- An investment property

- Shares

- Managed funds

- Commercial property

- Other investment assets

Importantly, CGT is not a separate tax.

Instead, the capital gain is added to your assessable income in the financial year the asset is sold.

This means a large capital gain can potentially increase your taxable income and affect the amount of tax payable for that year.

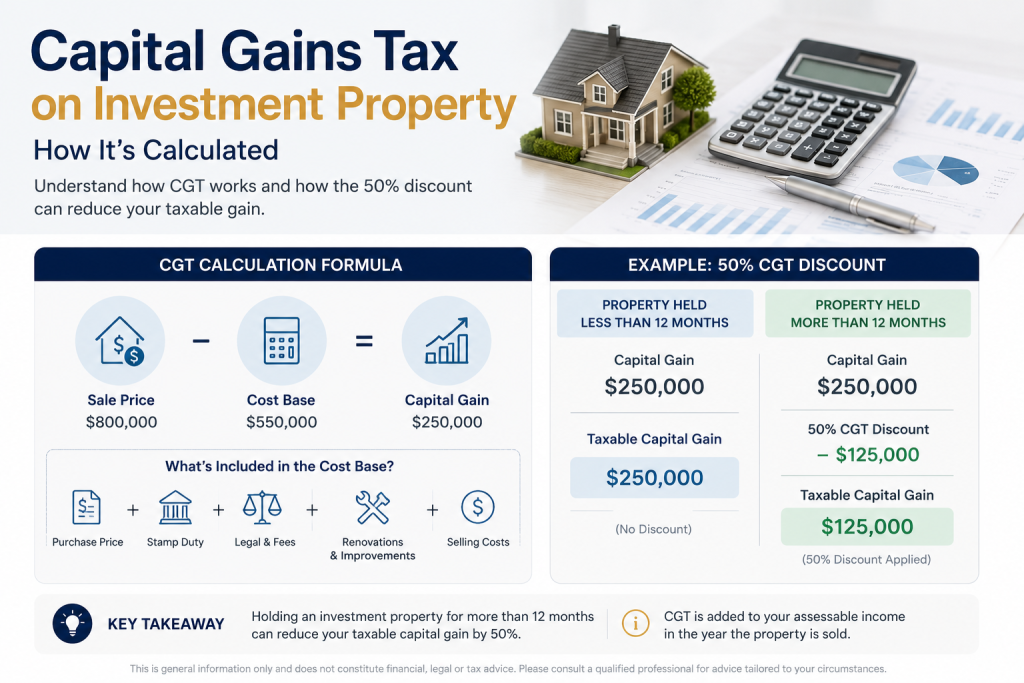

How is Capital Gains Tax Calculated?

The basic calculation is straightforward:

Capital Gain = Sale Price – Cost Base

However, determining the cost base is where many investors overlook potential deductions.

Your property’s cost base generally includes:

Purchase Costs

- Purchase price

- Stamp duty

- Conveyancing and legal fees

- Building and pest inspections

Ownership Costs

In certain circumstances:

- Interest expenses

- Council rates

- Land tax

- Insurance costs

Capital Improvement Costs

- Renovations

- Extensions

- Structural improvements

- New kitchens or bathrooms

Selling Costs

- Real estate agent commissions

- Marketing costs

- Legal fees associated with the sale

The higher your cost base, the lower your potential capital gain.

This is why accurate record keeping is critical throughout the life of your investment.

Capital Gains Tax Australia Investment Property: Understanding the 50% CGT Discount

One of the most valuable tax concessions available to Australian property investors is the 50% Capital Gains Tax discount.

If an individual investor or trust owns an investment property for more than 12 months before selling, only 50% of the capital gain may be included in their taxable income.

Example

Imagine you purchased an investment property and later sold it, generating a net capital gain of $200,000.

Held for Less Than 12 Months

Taxable Capital Gain = $200,000

The full amount is added to your taxable income.

Held for More Than 12 Months

50% CGT Discount Applies

Taxable Capital Gain = $100,000

Only half the gain is included in your assessable income.

This discount can significantly reduce the overall tax impact of selling an investment property.

How Negative Gearing and Capital Gains Tax Work Together

Successful investors often consider both negative gearing and capital gains tax Australia investment property outcomes when building a long-term portfolio. Negative gearing and CGT are often two parts of the same long-term investment strategy.

Phase 1: The Holding Period

During ownership, the property’s rental income may not fully cover expenses such as:

- Mortgage interest

- Property management fees

- Council rates

- Insurance

- Maintenance costs

This creates a rental loss which may potentially be used to offset other taxable income, subject to your individual circumstances.

Phase 2: Capital Growth

Over time, investors hope the property increases in value while tenants help contribute towards the property’s holding costs.

Phase 3: The Exit Strategy

When the property is sold, the investor may realise a significant capital gain.

If the property has been held for more than 12 months, the investor may qualify for the 50% CGT discount.

The ultimate goal for many investors is that the long-term capital growth significantly exceeds the short-term holding costs.

This is why understanding both negative gearing and capital gains tax on investment property in Australia is critical when building a property portfolio.

Which Properties Are Exempt from Capital Gains Tax?

Not every property sale results in a CGT liability.

Main Residence Exemption

In many circumstances, your principal place of residence (PPOR) is exempt from Capital Gains Tax.

Eligibility depends on:

- How the property has been used

- Whether it has generated rental income

- The period of ownership

- Your personal circumstances

Personal Use Assets

Generally exempt assets include:

- Motor vehicles

- Personal belongings

- Household furniture

Investment properties, commercial property and shares are generally subject to CGT rules.

Understanding the Six-Year Rule

Many Australian property owners are unaware of the ATO’s six-year rule.

If you move out of your primary residence and convert it into an investment property, you may still be able to treat it as your principal place of residence for CGT purposes for up to six years.

Depending on your circumstances, this could potentially provide significant tax benefits when selling.

Professional tax advice should always be sought before relying on this strategy.

3 Strategies That May Help Reduce Your CGT Liability

1. Keep Detailed Records

Good record keeping can make a substantial difference when calculating your capital gain.

Keep records for:

- Purchase costs

- Renovations

- Improvements

- Legal fees

- Stamp duty

- Selling costs

Every eligible cost included in your cost base may reduce your taxable gain.

2. Consider Timing Carefully

Because capital gains are added to your taxable income, the timing of a sale can influence the tax outcome.

Some investors choose to sell during periods when their income is lower.

Examples include:

- Retirement

- Career breaks

- Maternity or parental leave

- Reduced working hours

Always seek professional advice before making decisions based on tax outcomes.

3. Structure Your Finance Strategically

The way an investment loan is structured can influence your overall property investment strategy.

Working with an experienced mortgage broker can help ensure your lending structure aligns with your long-term investment goals.

Understanding capital gains tax Australia investment property implications before selling can help investors make more informed financial decisions and avoid unexpected tax outcomes.

Should You Sell or Hold?

One of the most common questions property investors ask is:

“Should I sell now or keep holding the property?”

The answer depends on several factors, including:

- Current market conditions

- Future growth expectations

- Cash flow requirements

- Tax implications

- Investment goals

- Borrowing capacity

A property that no longer aligns with your financial objectives may be worth reviewing.

However, selling purely for tax reasons is rarely the best strategy.

The decision should always be based on your broader financial goals.

Final Thoughts

Negative gearing may help support an investment property during ownership, but Capital Gains Tax is often where the financial outcome of the investment is ultimately realised.

Understanding how capital gains tax on investment property in Australia works can help investors make more informed decisions about buying, holding, refinancing and selling property.

A successful property investment strategy requires both a clear entry strategy and a clear exit strategy.

The earlier you understand how CGT affects your investment decisions, the better positioned you’ll be to build long-term wealth.

Thinking About Buying, Refinancing or Selling an Investment Property?

At Be Smart Finance, we help Australian property investors structure lending solutions that support both immediate cash flow requirements and long-term wealth creation goals.

Whether you’re purchasing your first investment property, expanding your portfolio, refinancing existing loans or reviewing your investment strategy, we’re here to help.

Book Your Free Investment Loan Review

📞 +61 408 659 819

📧 abhishek@besmartfinance.com.au

Discover lending solutions designed to support your property investment goals.

FAQ: Capital Gains Tax (CGT) on Australian Investment Properties

CGT is the tax that may apply when you make a profit from selling an asset such as an investment property, shares, managed funds, or commercial property. It is not a separate tax; instead, the capital gain is added to your taxable income in the financial year the asset is sold.

The basic formula is:

Capital Gain = Sale Price – Cost Base

The cost base may include:

- Purchase price

- Stamp duty

- Legal and conveyancing fees

- Building and pest inspections

- Certain ownership costs

- Capital improvements and renovations

- Selling costs such as agent commissions and marketing expenses

A higher cost base generally reduces your taxable capital gain.

If an individual or trust owns an investment property for more than 12 months before selling, only 50% of the capital gain may be included in taxable income.

Example:

- Capital gain: $200,000

- Held longer than 12 months

- Taxable gain: $100,000

This can significantly reduce the tax payable on the sale.

Negative gearing and CGT often work together as part of a long-term investment strategy:

- The property may generate tax-deductible losses during ownership.

- The property ideally appreciates in value over time.

- When sold, the investor may realize a capital gain and potentially qualify for the 50% CGT discount.

The strategy aims for long-term capital growth to outweigh short-term holding costs.

Potential cost-base items include:

- Purchase costs

- Stamp duty

- Legal fees

- Renovations and extensions

- Structural improvements

- New kitchens and bathrooms

- Real estate agent commissions

- Marketing expenses

- Sale-related legal fees

Keeping detailed records is essential.

In many circumstances, a principal place of residence (PPOR) may be exempt from CGT. Eligibility depends on:

- How the property was used

- Whether it produced rental income

- The ownership period

- Your personal circumstances

Specific advice should be obtained for individual situations.

Generally, no. Investment properties are usually subject to CGT rules when sold.

Examples may include:

- Motor vehicles

- Personal belongings

- Household furniture

Investment assets such as rental properties and shares are generally not exempt.

Accurate records help substantiate:

- Purchase expenses

- Improvement costs

- Ownership expenses

- Selling expenses

These records may increase the property’s cost base and reduce the taxable capital gain.

CGT is generally assessed in the financial year in which the asset is sold and the capital gain is realized. The gain is included in your assessable income for that year.

The guide notes that many Australian property investors use the six-year rule as part of their tax planning strategy. The specific application depends on individual circumstances and how the property is used over time.

Before selling an investment property, investors should consider:

- Potential CGT liability

- Eligibility for the 50% discount

- The property’s cost base

- Timing of the sale

- Overall tax position for the financial year

Professional tax advice can help optimize the outcome.