Table of Contents

ToggleBest Refinance Rates Australia – April 2026 Market Breakdown

Best Refinance Rates Australia are currently starting as low as 5.44% for eligible borrowers in April 2026, yet many homeowners are still paying 6.50% or more on their existing loans.This gap is often referred to as the “loyalty tax,” where long-term customers end up paying higher interest rates than new borrowers. In a high-rate environment shaped by the Reserve Bank of Australia, reviewing your mortgage and switching to a more competitive lender could save you thousands each year.

What the ASX RBA Rate Tracker is Telling Us

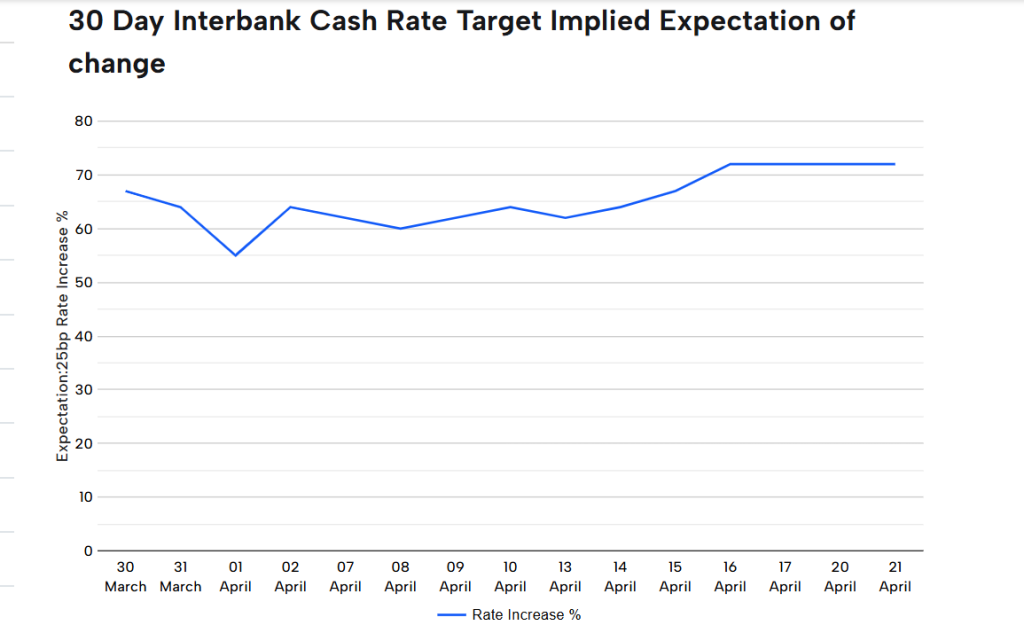

Understanding where the market is headed is crucial for any refinancing strategy. The ASX RBA Rate Tracker currently indicates a high level of uncertainty for the remainder of 2026:

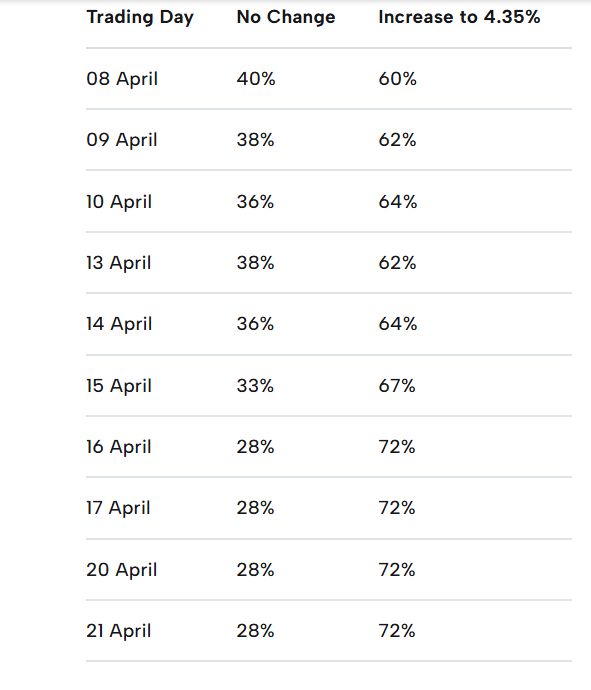

- 72% Expectation of a Hike: As of late April, market futures suggest a strong possibility that the RBA will increase the cash rate to 4.35% at the next meeting on May 5th.

- The “Hold” Scenario: Only 28% of the market predicts rates will stay at the current 4.10%.

With the probability of another hike looming, locking in the best refinance rates in Australia now is a proactive move to hedge against rising monthly repayments.

The Current Market: Top Refinance Offers in April 2026

The interest rate you are offered depends heavily on your Loan-to-Value Ratio (LVR). Generally, the more equity you have in your home, the lower the rate you can secure.

| Lender Category | Competitive Variable Rate | Best For |

|---|---|---|

| Leading Credit Unions | 5.44% - 5.64% | Borrowers seeking personalized service |

| Digital/Online Lenders | 5.08% - 5.69% | Tech-savvy owners with high equity (LVR < 60%) |

| Major Banks (Big 4) | 5.74% - 6.14% | Those who prioritize brand stability |

Note: The absolute lowest rates (near 5.08%) are often reserved for “ultra-low” LVRs of 50% or less.

The Real Savings: Why Refinancing Matters

Let’s look at the math for a typical $600,000 Australian mortgage:

- Current “Loyalty” Rate (6.75%): Repayment is approx. $3,892/month.

- New Refinance Rate (5.50%): Repayment is approx. $3,407/month.

- Total Savings: $485 per month or $5,820 per year.

That is nearly $6,000 back in your pocket—money that could be redirected toward your superannuation, school fees, or paying off your loan principal faster.

Fixed vs. Variable: Which Strategy Wins in 2026?

Given the 72% chance of a rate hike predicted by the ASX Tracker, many Australian borrowers are moving away from “set and forget” variable loans toward a Split Loan Strategy:

- Fixed Portion (e.g., 60%): Protects you from the potential climb to 4.35% or higher.

- Variable Portion (e.g., 40%): Allows you to use an Offset Account to lower interest and maintain the flexibility to redraw funds if needed.

Get a Professional Home Loan Health Check

Finding the best refinance rates in Australia involves more than just looking at the headline number. You must also consider exit fees, application costs, and whether a lender’s features (like multiple offset accounts) align with your lifestyle.

At BeSmart Finance, we simplify this process by:

- Comparing over 30+ lenders in one session.

- Identifying “hidden” loyalty taxes on your current loan.

- Managing the entire paperwork process from application to settlement.

Stop paying more than you have to. With the RBA meeting just around the corner, now is the time to see if your current loan still makes sense.

FAQs: Best Refinance Rates Australia (2026 Guide)

As of April 2026, refinance rates in Australia start from around 5.08% for borrowers with low LVR.

Yes, refinancing can save borrowers over $5,000 annually depending on their current rate and loan size.

Lower LVR (more equity) usually qualifies you for better interest rates.

With rising rate expectations, many borrowers are choosing split loans for flexibility and protection.